Tax Consequences Resulting From Foreclosure On A Reverse Mortgage

Doesnt pay taxes or insurance. If you cant do either you can provide the lender with a deed in lieu of foreclosure.

All About Reverse Mortgage Alok Surana

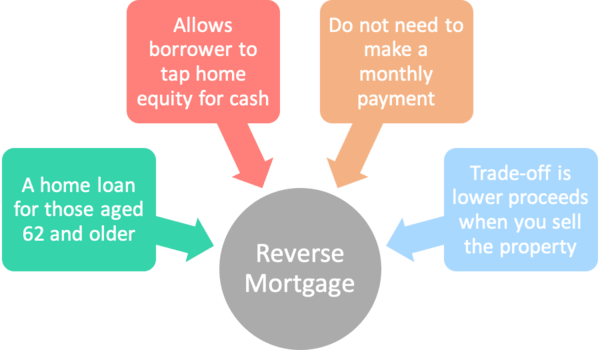

With a reverse mortgage loan payment does not become due until the borrower.

Tax consequences resulting from foreclosure on a reverse mortgage. Do you feel you were taken advantage of by your Loan Servicer when you took out a Reverse mortgage in city state. Is interest on a reverse mortgage tax deductible. Its the natural resolution of a reverse mortgage after the borrower passes away.

Reverse mortgage contracts can have hidden costs such as fees and interest can eat up your home equity. This is why most people view it with distaste look askance at the lenders who. Therefore a 22 million capital gain would be recognized resulting from the difference between the loan balance of 30 million and the remaining tax basis of 8 million.

If the property is deeded to the mortgage company or purchased at the foreclosure auction by mortgagee you will have no income tax liability. This is a result of the unique conduit taxation nature of an estate. More often a foreclosure forces borrowers to move from their home.

On a forward mortgage foreclosure arises from failure of the borrower to make required monthly payments of principal and interest and it almost always involves a forcible eviction. Credit and Tax Implications. A deed in lieu of foreclosure is sufficient to extinguish the debt on the reverse mortgage.

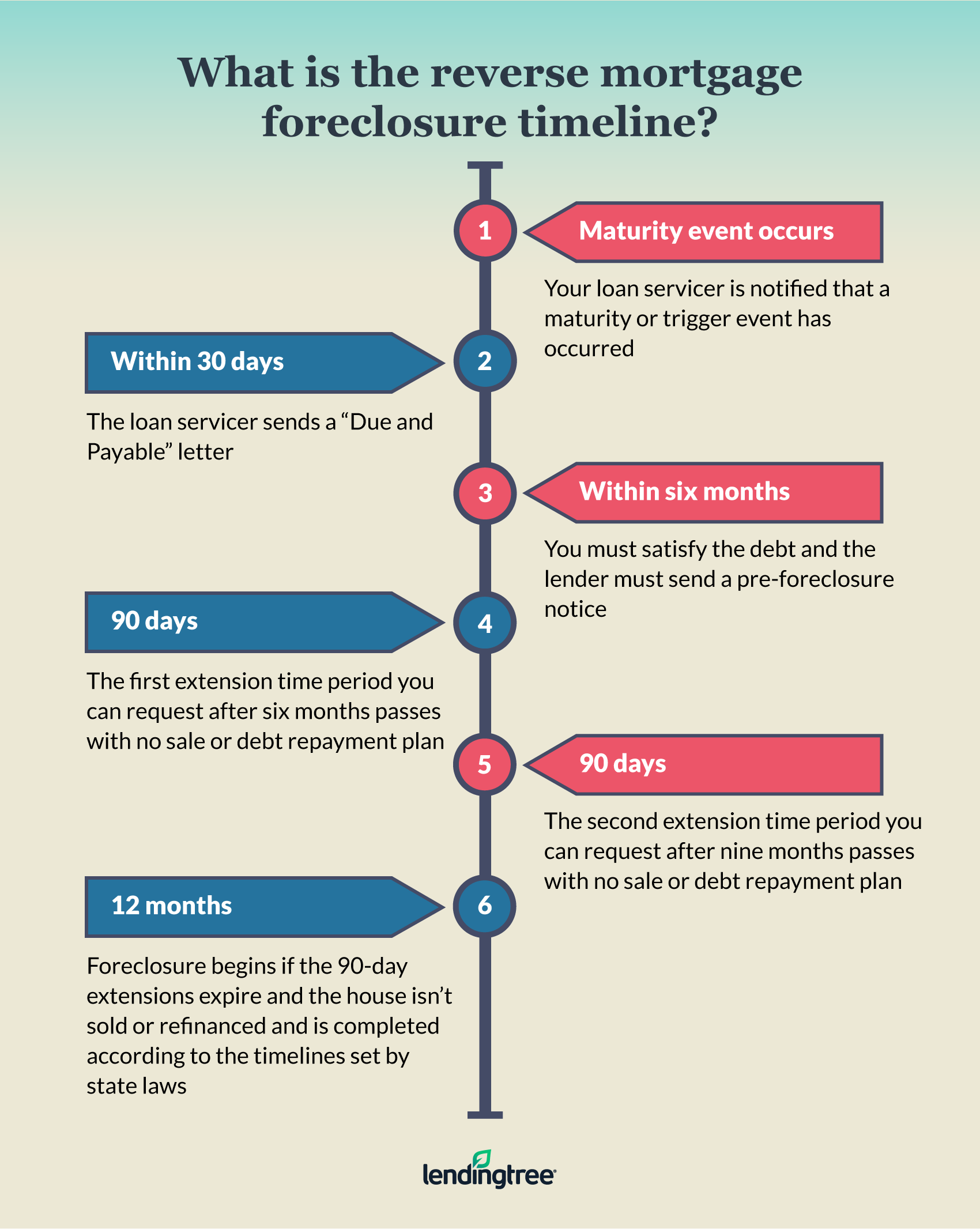

Reverse mortgage foreclosure typically happens when. When a lender forecloses a borrower is forced to pay back a reverse mortgage. You must continue to pay for repairs property insurance and taxes.

The lender pays you the borrower loan proceeds in a lump sum a monthly advance a line of credit or a combination of all three while you continue to live in your home. If you are unsure of your rights and responsibilities you should consult a lawyer in your area who is experienced in both. There is no next of kin to handle a sale.

Even though reverse mortgages dont require a monthly principal and interest mortgage payment during the life of the loan there are other borrower obligations contained. The Tax Implications of a Reverse Mortgage LendingTree. This capital gainsubject to recapture rules would pass through to each partner on their K-1s.

If a third party purchaser buys the property for more than your basis you will have to pay capital gains tax on the profit you make. As stated above cancellation of debt income is not taxable in the case of non-recourse loans A reportable gain from the disposition of the home because foreclosures are treated like sales for. Reverse mortgage tax issues.

Fails to follow the loans guidelines. In addition the interest has to meet the other rules for deducting home mortgage interest. This article does not address the income tax consequences of.

Mortgage insurance from the government will compensate the lender for the difference. If you are a reverse mortgage borrower who decides to move out of your home you are still responsible for paying off the loan or selling the house for at least 95 of its appraised value. From a tax standpoint a non-recourse loan foreclosure is treated as if the property was sold for the remaining balance of the loan.

Any partners who have outside basis could then apply their portion to their capital gain. Thus foreclosures on a reverse mortgage mean something entirely different than foreclosures on a forward mortgage. Thus foreclosures on a reverse mortgage mean something entirely different than foreclosures on a forward mortgage.

Under the current tax law home equity debt is only. September 26 2018 New York Foreclosure Defense Leave a comment Andres Cardenas Buying A Reverse Mortgage Foreclosure Defenses To Reverse Mortgage Foreclosure Foreclosure On Reverse Mortgage Help With Reverse Mortgage. Reverse mortgage payments are considered loan proceeds and not income.

One of the most important reverse mortgage tax consequences has to do with capital gains taxesCapital gains taxes are the taxes you pay when you sell a capital asset such as real estate stocks or other investments. This is why most people view it with distaste look askance at the lenders who. Unless you are careful you can risk losing your home or have it.

When one of. You can only deduct interest on a reverse mortgage when its paid. As a reminder from a tax perspective an estate is sometimes referred to as a pass-through entity.

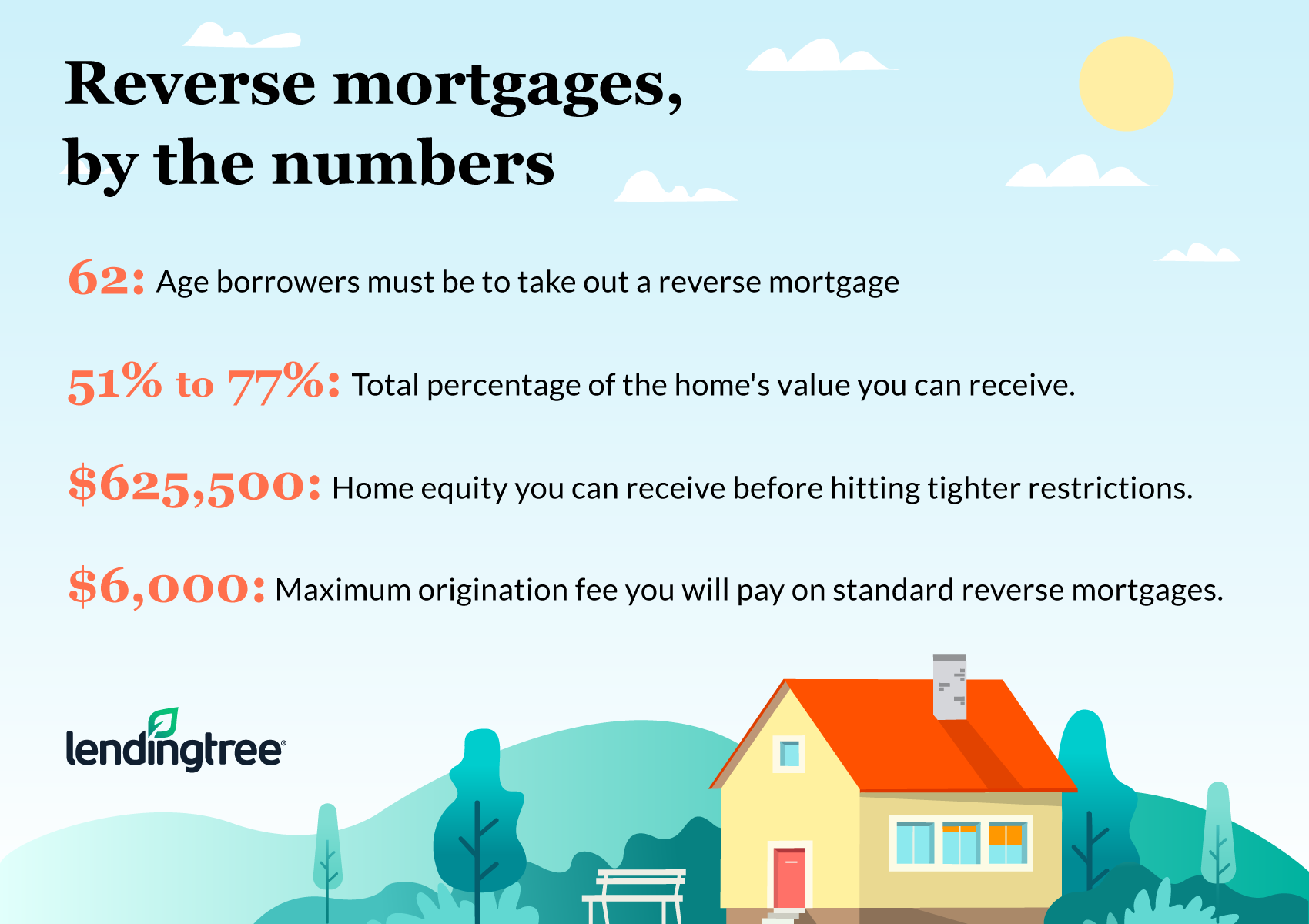

On a forward mortgage foreclosure arises from failure of the borrower to make required monthly payments of principal and interest and it almost always involves a forcible eviction. When you take out a reverse mortgage the title to your home remains with you and you continue to live in the home. Reverse mortgages come with more regulations than a regular mortgage so that accounts for some of the additional fees.

Does not maintain the property. The balance due exceeds the homes value. Although signing a deed in lieu of foreclosure may protect your credit or that of your heirs it does not extend the same protection to income taxes.

No reverse mortgage payments arent taxable. Reverse Mortgage Foreclosure Tax Consequences. Tax Consequences Resulting from Foreclosure on a Reverse Mortgage One of the most perplexing aspects of the Home Equity Conversion Mortgages HECMs is the income tax consequences of forgiving or canceling any portion of the balance due through short sale foreclosure trustees sale or deed in lieu of foreclosure.

Since most reverse mortgages arent paid until the home is sold or the borrower dies you may never benefit from the tax deduction. Taxable cancellation of debt income. With both types of loan foreclosure ultimately results in the transference of a homes title from the borrower to the bank.

If any portion of. With a reverse mortgage you retain title to your. When you move out sell the home or die or the last surviving borrower dies you or your estate will need to repay the loan.

Reverse Mortgage Foreclosure. There are two possible consequences you must consider. Lenders also charge more because they claim they take on unique risks in that reverse mortgages arent based on your income or credit score29 2019 .

Is subject to an underwater reverse mortgage that is then foreclosed and the mortgage company discharges the remaining debt.

How To Germany Mortgages In Germany

What Are The 3 Types Of Reverse Mortgages Explained Goodlife

Reverse Mortgages Who They Re For And The Pros And Cons

Reverse Mortgage Alternatives 5 Options For Seniors Credible

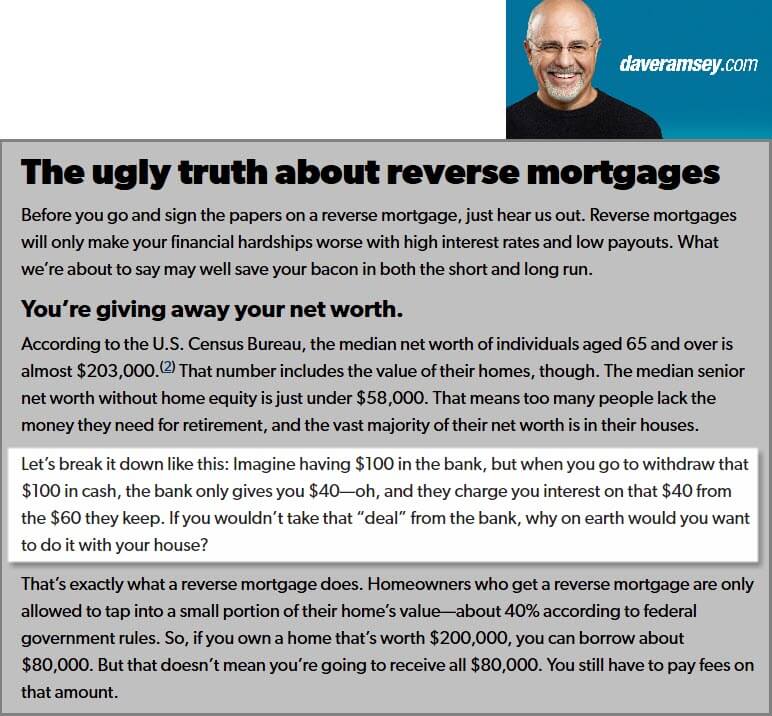

Dave Ramsey Offering Bad Advice On Reverse Mortgages

Reverse Mortgage Foreclosure Lendingtree

Reverse Mortgage Loans A Quantitative Analysis Nakajima 2017 The Journal Of Finance Wiley Online Library

9 Key Reverse Mortgage Questions Answered Lendingtree

Infographic How Would Federal Tapering Affect Me Lender411 Com Economy Infographic Mortgage Interest Rates Mortgage Payoff

Pdf Reverse Mortgages Financial Inclusion And Economic Development Potential Benefit And Risks Reverse Mortgages Financial Inclusion And Economic Development Potential Benefit And Risks

Reverse Mortgages And Foreclosures Loan Lawyers

Consumer Lending Discrimination In The Fintech Era Sciencedirect

Pdf Reverse Mortgages Financial Inclusion And Economic Development Potential Benefit And Risks Reverse Mortgages Financial Inclusion And Economic Development Potential Benefit And Risks

What Is A Reverse Mortgage And How Does It Work Money

Reverse Mortgage Problems Myths And Truths Homeequity Bank

Danish Covered Bonds 2020 2021 Nykredit Markets

What Are The 3 Types Of Reverse Mortgages Explained Goodlife

Learn How A Reverse Mortgage Works In 2021 Arlo

The Truth About Reverse Mortgage Foreclosure Rmf

{kind=link}

Posting Komentar untuk "Tax Consequences Resulting From Foreclosure On A Reverse Mortgage"